Those who are struggling with recording contra accounts may benefit from utilizing some of the best accounting software currently available. When accounting for assets, the difference between the asset’s account balance and the contra account balance is referred to as the book value. There are two major methods of determining what should be booked into a contra account. By keeping the original dollar amount intact in the original account and reducing the figure in a separate account, the financial information is more transparent for financial reporting purposes.

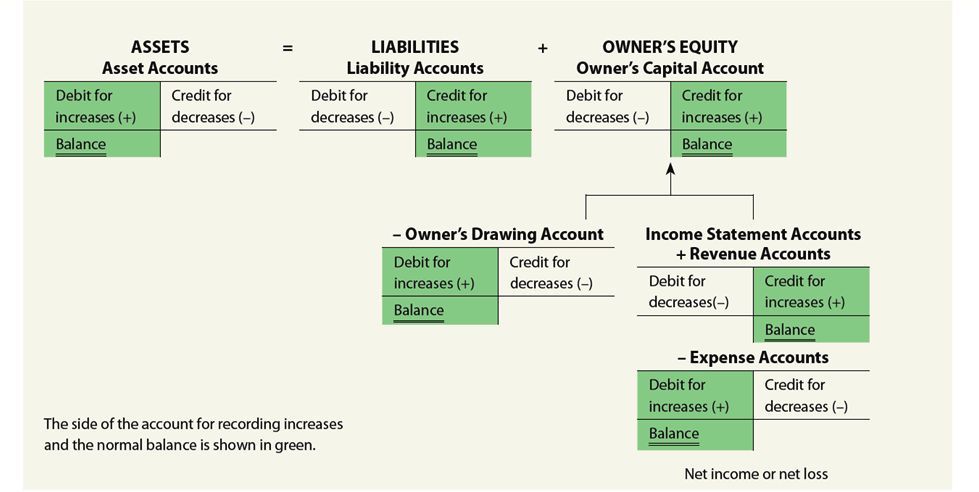

Revenues and Gains Are Usually Credited

It will debit Accounts Receivable for $100,000 and will credit Sales for $100,000. If a customer returns $500 of this merchandise, Company K will debit Sales Returns and Allowances for $500 and will credit Accounts Receivable for $500. On the balance sheet, a contra account is typically used to reduce the book value or historical value of an asset or liability. A contra revenue account is a revenue account that is expected to have a debit balance (instead of the usual credit balance).

What is the difference between a contra account and a regular account?

Therefore, for these three, the debit balance actually represents a negative amount. The sales discounts contra revenue account records the discounts given to customers on sales made to them, normally a cash or settlement discount. The account is normally a debit balance and in use is offset against the revenue account which is normally a credit balance. Consequently the net balance of the two accounts shows the net value of the sales after discounts. A liability recorded as a debit balance is used to decrease the balance of a liability. It is not classified as a liability since it does not represent a future obligation.

Contra Account Explained

Contra liability accounts are used to offset the balance in a liability account. For example, if a company has a liability account for unearned revenue, they would also have a contra the usual balance in a contra-revenue account is a: liability account to offset the balance in the unearned revenue account. Contra accounts are used in accounting to provide a more accurate picture of a company’s financial position.

Do Contra Accounts Have Debit or Credit Balances?

The Allowance for Doubtful Accounts is used to track the estimated bad debts a company my incur without impacting the balance in its related account, Accounts Receivable. An estimate of bad debts is made to ensure the balance in the Accounts Receivable account represents the real value of the account. Allowance for Doubtful Accounts pairs with the Bad Debts Expense account when doing adjusting journal entries. A delivery van is purchased by a business to use in delivering product and picking up materials.

- A contra asset account is an asset account where the account balance is a credit balance.

- The balance in the allowance for doubtful accounts represents the dollar amount of the current accounts receivable balance that is expected to be uncollectible.

- For companies in the business of lending money, Interest Revenues are reported in the operating section of the multiple-step income statement.

- When a contra asset account is first recorded in a journal entry, the offset is to an expense.

- Contra accounts are used to record adjustments, reversals, or reductions in the value of assets or liabilities.

What is a Contra Account?

Contra accounts are typically used to show the credit balance of an account that has a debit balance, and vice versa. Accruing tax liabilities in accounting involves recognizing and recording taxes that a company owes but has not yet paid. This is important for accurate financial reporting and compliance with… These accounts can be listed based on the respective asset, liability, or equity account to reduce their original balance.

It ensures that financial statements accurately reflect a company’s financial position. For instance, the “Accumulated Depreciation” contra account offsets the value of fixed assets like machinery or buildings, reflecting their reduced value over time due to wear and tear. A contra asset is paired with an asset account to reduce the value of the account without changing the historical value of the asset.

A contra revenue account allows a company to see the original amount sold and to also see the items that reduced the sales to the amount of net sales. Equity recorded as a debit balance is used to decrease the balance of a standard equity account. It is a reduction from equity because it represents the amount paid by a corporation to buy back its stock. The contra account accounting reduces the total number of outstanding shares. The treasury stock account is debited when a company buys back its shares from the open market. Examples of contra accounts include accumulated depreciation, allowance for doubtful accounts, and sales returns and allowances.